If you are trying to decide which is the best way to move your money abroad (or receive money from another country), this article Money Transfer Companies Compared is exactly what you need.

Below are all the different options for making international money transfers. We'll help you with some common questions like:

- Which is better, WorldRemit, WorldFirst, TransferGo or CurrencyFair?

- How do currency brokers like OFX compare to CurrencyFair?

- Are banks much more expensive than CurrencyFair?

- CurrencyFair vs TransferWise?

- Revolut vs TransferWise?

- CurrencyFair v Paypal

- Which provider is the best peer to peer currency exchange?

Money Transfer Companies Compared

Let the comparisons begin! In this article, we compare CurrencyFair to:

- AIB

- An Post

- Azimo

- Bank of Ireland

- Barclays

- Halifax

- HSBC

- KBC

- Lloyds Bank

- MoneyCorp

- Monzo

- N26

- Nationwide

- NatWest

- Neteller

- OFX

- PayPal

- Permanent TSB

- Post Office (UK)

- Remit2India

- Revolut

- Royal Bank of Scotland (RBS)

- Skrill

- Starling

- The Co-operative Bank

- TransferGo

- TransferWise

- Travelex

- Ulster Bank

- Western Union

- WorldFirst

- WorldRemit

- XE.com

- Xoom

AIB

As CurrencyFair is Irish-based company (with offices worldwide) we want to include Irish banks that offer currency exchange online in our comparison along with bigger international providers.

Allied Irish Banks (AIB) is one of the so-called “Big Four” banks in Ireland. Within their website, AIB list the exchange rates they are selling currencies at for international payment, clearly stating that the rates are updated daily:

(Gathered on 18 November 2019 at 11:09)

(Comparison carried out on 18 November 2019 at 11:21)

(Comparison carried out on 18 November 2019 at 11:21)

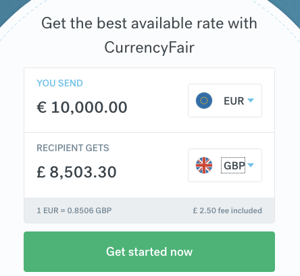

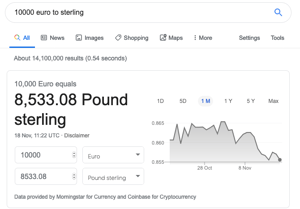

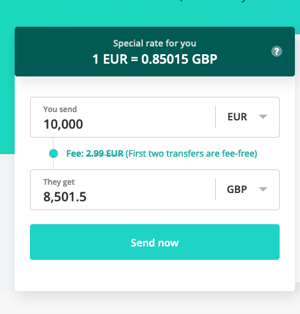

At the time of the comparison (11.21AM on the 18 November 2019), the exchange rate on offer with CurrencyFair to exchange Euro to Pound Sterling was 0.8506. The exchange rates listed by AIB on the 18 November 2019 to exchange Euro to Pound Sterling. AIB were offering 0.8426, a rate set at 07.30 AM at the day of the comparison. These rates are subject to change.

To exchange €10 000 with CurrencyFair, would have send £8 503.30 to the recipient including our £2.50 fee– just £29.78 away from the currency market rate of £8 533.08. This is compared to what an exchange of €10 000 was with AIB at the time; approximately £8 426 for the recipient before fees–that’s over £77 less than with the final cost with CurrencyFair.

(Comparison carried out on 18 November 2019 at 11:21)

That’s because we offer live exchange rates based off the live currency market rate, so our customers are always getting the best available rates.

An Post

The new-look An Post has started marketing more financial products to Irish customers, who can avail of a currency card as well as standard forex cash services at participating outlets. For either option, both are advertised as “commission-free or “0% commission” throughout the An Post website.

(Gathered on 18 November 2019 at 11:36)

Interestingly, An Post advise that their rate to exchange currencies via their stores or currency card is “more advantageous” than to swop currencies than online.

(Gathered on 18 November 2019 at 11:47)

Let’s look to see if this is true. A basic comparison on the 18 November 2019 shows:

(Comparison carried out on 18 November 2019 at 11:59)

(Comparison carried out on 18 November 2019 at 12:00)

(Comparison carried out on 18 November 2019 at 11:23)

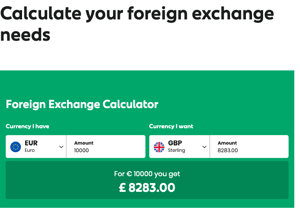

Comparing the EUR-GBP exchange rates, CurrencyFair offered 0.8506, the currency market rate is 0.8533 and the daily set exchange rate with An Post is 0.8283–the An Post rate is almost 3% less than what the EUR-GBP exchange rate on offer with CurrencyFair was at the time of the comparison.

Which begs the question: why advise customers that the An Post rate to exchange currencies via their stores or currency card is “more advantageous” than to swop currencies than online?

In this example above, it was not the case.

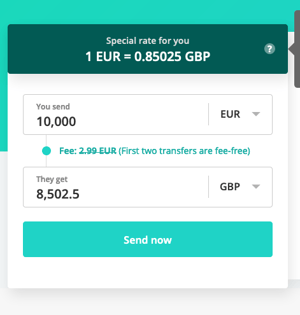

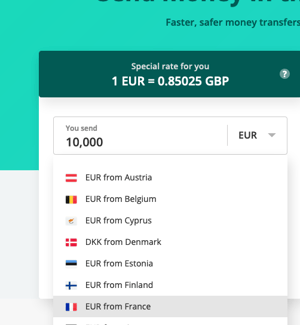

Azimo

The Azimo mission is similar to CurrencyFair–to “use technology to democratise financial services, making them affordable and available to all.”

For CurrencyFair customers this is simply currency exchange without compromise.

Azimo pricing is advertised as a “special” exchange rate. The final amount a recipient receives when transferring €10,000 to the United Kingdom using Azimo changes depending on the country the Euro is being sent from. Sending Euros from Austria? The recipient receives a different amount, depending on their country.

(Comparison carried out on 18 November 2019 at 14:23)

(Comparison carried out on 18 November 2019 at 14:24)

(Comparison carried out on 18 November 2019 at 14:24)

With CurrencyFair, customers exchange Euros at the best available rates, no matter the EU country they are transferring Euros from.

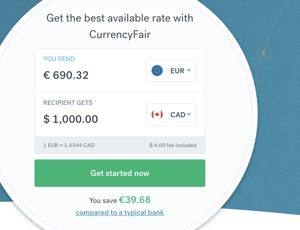

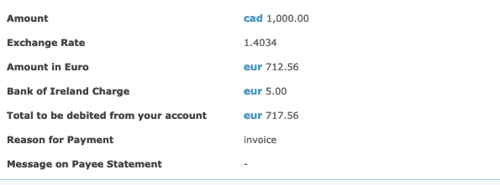

Bank of Ireland

Bank of Ireland is another one of the “Big Four”. As the oldest bank in operation in Ireland, it has branches nationwide, offering forex services for both personal and business accounts.

To exchange Euro to Canadian Dollars with CurrencyFair, the exchange rate was seen at 1.4544 at the time of the comparison. The rate at the same time on the Bank of Ireland currency calculator as well as when logging into a personal account (as we were able to do) showed a rate of 1.4034 at that time.

(Comparison carried out on 18 November 2019 at 14:36)

(Comparison carried out on 18 November 2019 at 14:35)

That’s an almost 4% difference between the rate received with CurrencyFair and the rate received with Bank of Ireland. This is again an example of how traditional providers may say they offer free transfers or “0% commission transfers” but in reality, a mark-up is hidden in the exchange rate given to customers.

In this example, to exchange €10 000 to Canadian Dollars, gives you C$14 544 with CurrencyFair and C$14 034 with Bank of Ireland. That’s a difference of C$510 before fees–our fee to transfer CAD to a bank account in Canada is then just C$4.

Barclays

Like many traditional banks and financial service providers, Barclays claims that “sending money is fee-free” online.

(Gathered on 18 November 2019 at 14:50)

Indeed–the fee to complete online banking is free. But upon further investigation, we found an overseas collection charge is deducted from an account when transferring to other countries outside of the UK. £6 is charged on behalf of the recipient by Barclays when sending money to Canada.

(Gathered on 18 November 2019 at 14:51)

The fee to transfer money to a bank account overseas is just €3 or the currency equivalent with CurrencyFair–for money transfers of all sizes.

Halifax

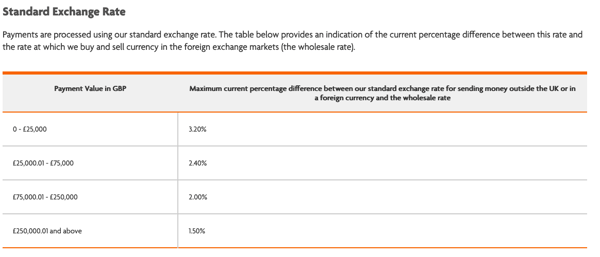

Halifax are up front with their charges: £9.50 for an online money transfer and paying anywhere from £12–£20 for the correspondent bank fee, if there is any. In addition, Halifax also outline their margin to be, as they explain it,

“...the percentage difference between this rate and the rate at which we buy and sell currency in the foreign exchange markets (the wholesale rate).”

Meaning for transfers between £0 and £25 000 there is a maximum of 3.2% added onto their standard exchange rate compared with the currency market rate. Their next transfer bracket is £25 000 to £75 000 and then the percentage margin actually drops to 2.4%. Halifax clearly explain the breakdown of the margin added to theirs exchange rates.

(Gathered on 18 November 2019 at 16:44)

In comparison, CurrencyFair adds a margin that is typically just 0.45% away from the currency market rate. Then our fee to transfer money to a bank account is €3 (or the currency equivalent).

HSBC

HSBC is one of the largest banks in the world with a market capitalisation of over £120 billion. While they advocate for simplicity when it comes to their fees, their foreign exchange rates are more tricky to work out. Fees charged by HSBC for an international money transfer is £4.

(Gathered on 18 November 2019 at 16:44)

In their terms and conditions, global payments are given a special exchange rate separate to other FX services, and can be changed “immediately and without giving advance notice”.

When completing an international money transfers with HSBC or any banking provider, be sure to compare the rate offered with the currency market rate at the same time. This is where a hidden markup can be added by providers to the exchange rate, meaning customers receive less on their exchange.

Our calculator shows the real-time cost with CurrencyFair of a transfer–our exchange rate and our £2.50 fee to transfer the exchanged money. We also highlight any third-party fees that customers could be exposed to if and when needed so the cost of a money transfer is clear at every step.

KBC

KBC operate through numerous “hubs” across Ireland. Their site offers a dedicated foreign exchange page but no listed exchange rates.

Currency exchange fees are not listed in their fees and charges PDF either so forex seems to not be a service currently available to their customers.

However, customers can use their KBC debit card to make purchases in a foreign country on their card, with their charge for this service being 1.75%.

Lloyds

One of the “Big Four” banks in the UK, most of Lloyds bank branches are located in the United Kingdom and Wales.

In the same way as with Halifax (a subsidiary of the Lloyds group) above, their costs to send money globally are structured around a Correspondent Bank Fee. While it is free to send money via their MoneyMover service however a Correspondent Fee of £12–£20 can be applied

(Gathered on 21 November 2019 at 14:14)

The Lloyds website states that they offer a wide range of currency exchange rates–but it is stated that these “can change at any time.”

There is a limit to how much can be sent online from your account with the daily limit for an international money transfer with Lloyds Bank being the equivalent of £30 000.

(Gathered on 21 November 2019 at 14:15)

With CurrencyFair, our fee is just £2.50 (or the currency equivalent) to transfer out exchanged money and our customers don’t have a daily transfer limit on how much currency can be exchanged.

MoneyCorp

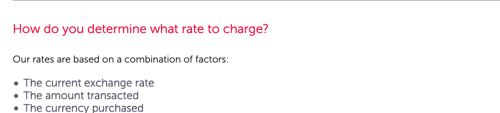

MoneyCorp is an international company which provides several foreign exchange services, including a bureau de change and online global payments platform.

MoneyCorp does not offer any indication of the margin applied to the exchange rates given to their customers. However the website states that “the current exchange rate, the amount transacted” as well as “the currency purchased” all play a part in the final amount received by the recipient.

(Gathered on 20 November 2019 at 10:12)

Our calculator allows users to get a true indication of not only our live exchange rate but our fees for our standard transfer in real-time. If using Faster Payments with CurrencyFair, GBP transfers can occur within the same day or one business day.

Monzo

A relatively younger provider to the international money transfer market, Monzo aims to build “the best current account on the planet”. A Monzo currency account has features like bill splitting, instant transfers to other users and free purchases with their card both in the UK and abroad.

The UK-based digital bank offers international transfers with TransferWise. See more below.

N26

N26 is another popular digital bank, based in Germany where it was founded in 2013. Contesting the traditional financial services, they also outsource international payments to TransferWise.

See more below.

Nationwide

Nationwide is the largest building society in the world with over 15 million members.

For currency exchange, the fee with Nationwide to send money within Europe is £9, while sending it further afield will incur a fee of £20.

(Comparison carried out on 18 November 2019 at 17:14)

(Comparison carried out on 18 November 2019 at 17:15)

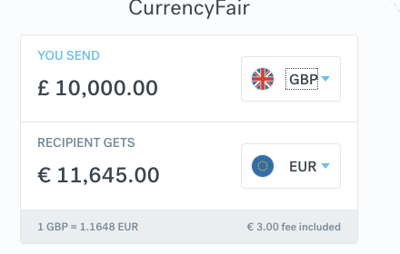

Nationwide do publish their exchange rates on their website. On the 18 November 2019 at 17:14, their daily GBP-EUR rate was 1.1453. With CurrencyFair at the same time, it was 1.1648. So before fees, to exchange £10 000 to Euro would result in €11 648 with CurrencyFair and approximately €11 453 with Nationwide–excluding fees–based on the rates seen on their website. Nationwide state that once customers login rates shown will differ from this. This means customers might be offered a slightly more accurate rate than a set daily one.

(Comparison carried out on 18 November 2019 at 17:14)

(Comparison carried out on 18 November 2019 at 17:15)

NatWest

NatWest, short for National Westminster, has been part of the Royal Bank of Scotland Group since 2000. Therefore their websites have a very similiar look, feel and even similar fees charged on money transfers.

In their Fees & Charges schedule published on 19 January 2019, the charge for sending money abroad with NatWest can range from £10 to £30 for anyone with their Select accounts, Reward accounts or with a Student, Graduate and Foundation account.

(Gathered on 25 November 2019 at 13:12)

For anyone with their Adapt account fees for SEPA and standard transfers are free and it costs £25 to process an urgent international transfer.

(Gathered on 18 November 2019 at 14:01)

To compare, the fee to transfer out Pound Sterling for a CurrencyFair customer is just £2.50–meaning our customers can transfer almost nine times with CurrencyFair for the price of a “Standard” international payment with NatWest. Then there are our excellent exchange rates, offering customers even more savings.

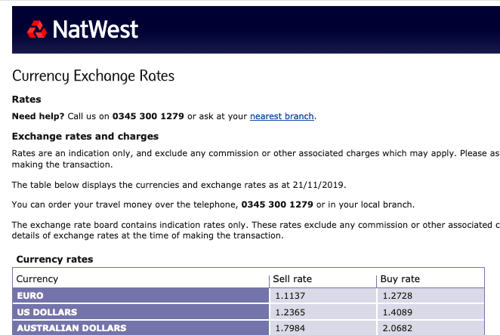

NatWest do publish a page with their daily exchange rate, but include the caveat:

(Gathered on 20 November 2019 at 10:22)

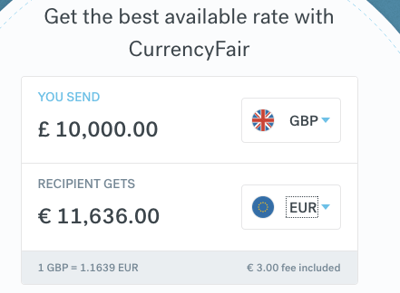

A quick comparison shows the rates to exchange GBP-EUR with NatWest to be 1.1137 and with CurrencyFair at the time of the comparison, the GBP-EUR rate is 1.1639. So to exchange of £10 000 with NatWest would result in approximately €11 137 before fees and to exchange of £10 000 with CurrencyFair would give €499 more–€11 636 including our €3 fee.

(Comparison data gathered on 21 November 2019 at 14:33)

(Comparison data gathered on 21 November 2019 at 14:33)

Neteller

Neteller offers payment solutions, such as prepaid Mastercards and mobile payments, but for comparison we’ll be looking at their overseas bank to bank transfer option only. Both the process of making a deposit or withdrawing from your Neteller account are subject to fees: “Uploads” are charged 2.5% of their value, while “Withdrawals” will cost 10 USD. The “price” for sending money online with Neteller is 1.45%.

(Gathered on 19 November 2019 at 11:41)

OFX

OFX, previously known as OzForex, operates from Australia offering global money transfers.

Their website shows that they offer “competitive transfer rates* ”. Using their live currency converter, OFX displays the “market rate”, not their “customer rate”–which is only shown when customers login or register.

(Gathered on 19 November 2019 at 11:46)

(Gathered on 19 November 2019 at 11:46)

With CurrencyFair our calculator shows the best available rates for customers, including our margin added to the (currency) market rate. Typically our margin is just 0.45% away from that rate meaning better value FX rates and more savings on money transfers for our customers.

PayPal

PayPal is a popular choice especially for online stores and ecommerce sites. However often their customers are in the dark as to how much and where they are being charged fees.

PayPal charge exchange rates that not only incorporate a margin but also their fees to convert money and to send this money across borders.

These fees and charges apply not just for personal accounts–businesses get charged exchange rates that are different again.

PayPal charge a “currency conversion fee” as well adding their mark-up to the exchange rates offered. This fee can vary from between 3% to 4% depending on the currency that is being sought.

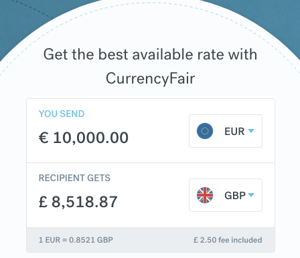

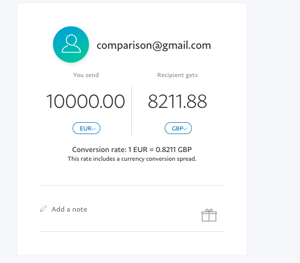

To quickly compare, a transfer of €10,000 to the UK from a Euro bank account, would give £306 less using PayPal. On the 19 November 2019, at 11:55 (GMT+1), a €10,000 transfer to the UK with PayPal would deliver £8 211.88. The equivalent transfer with CurrencyFair would give the recipient £8 518.87 including our one simple transfer free.

That’s £306.99 more for our customers to exchange €10 000 to Pound Sterling.

(Comparison carried out on 19 November 2019 at 12:03)

(Comparison carried out on 19 November 2019 at 12:03)

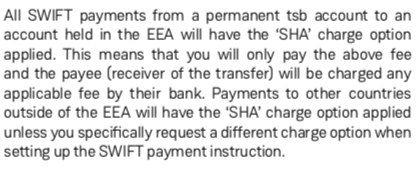

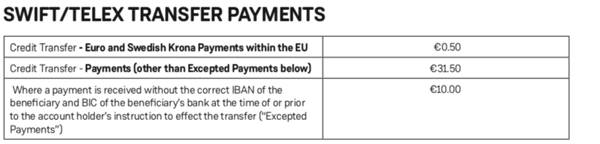

Permanent TSB

Permanent TSB is an Irish-based bank that offers foreign exchange to their personal account holders however they do not publish their rates or offer a free currency converter on their website.

In their Schedule of Fees & Charges published in March 2019, the fees for a money transfer of currencies other than Euro and Swedish Krona to areas outside the EU, the fees was €31.50.

(Gathered on 19 November 2019 at 13:21)

In contrast, the fee to transfer money with CurrencyFair is just €3 (or the currency equivalent).

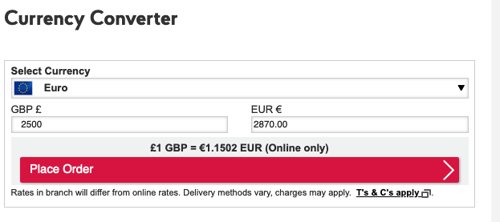

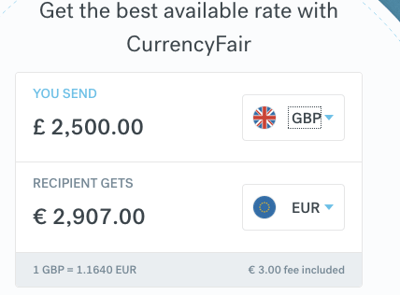

Post Office (UK)

Post offices all over the world have evolved from simply handling letters and selling stamps, to providing mortgages, credit cards and even motor insurance. They now also offer currency exchange, just like Post Office branches across the United Kingdom and Northern Ireland.

To compare with CurrencyFair, our rate to exchange £2 500 to Euros at the same time was approximately €2 907, while the Post Office was offering €2 870.

(Comparison carried out on 19 November 2019 at 15:00)

(Comparison carried out on 19 November 2019 at 15:02)

The UK Post Office also operates a worldwide cash transfer service with Western Union – more on them later.

Remit2India

Their percentage commission changes depending on the amount and the currency customers exchange from.

(Gathered on 20 November 2019 at 09:38)

For a limited time there is a free transfer offer for their customers that only applies “once your funds are received by remit2india.”

(Gathered on 20 November 2019 at 09:40)

(Gathered on 20 November 2019 at 09:39)

(Gathered on 20 November 2019 at 09:39)

(Gathered on 20 November 2019 at 09:39)

With CurrencyFair, our fee to transfer is typically 125 INR–along with our limited time offer of free INR transfers. Find out more here.

Revolut

Another popular alternative is Revolut: this provider offers a card solution and an app. Good for small transfers amounts. However Revolut have a cap on the volume of FX transfers they process for free every month. A Revolut customer can only transfer up to £5,000 / €6,000 or its currency equivalent per month for free. After reaching the limit of €6 000 Revolut’s fees start at €7.99 per month for their Premium account–that has no monthly limit.

When sending Sterling with CurrencyFair, we offer Faster Payments for outgoing transfers, funds will generally reach their destination in the same time-frame. And most importantly this service is offered by us at no extra cost – our standard CurrencyFair transfer fee of just £2.50 will still apply.

RBS

The Royal Bank of Scotland – or RBS – serves approximately 18.9 million members all over the world, and offers those customers the chance to send money abroad as one of their many “Ways to Bank”.

The charge for sending money abroad with RBS can range from £10 to £30 for anyone with their Select accounts, Reward accounts and a Student, Graduate, Foundation account.

(Gathered on 25 November 2019 at 14:01)

For anyone with their Revolve account fees for SEPA and standard transfers are free and it costs £25 to process an urgent international transfer.

(Gathered on 25 November 2019 at 14:01)

While the fees for sending money abroad are available on the RBS website, foreign exchange rates are a little more unclear and only offered for buying bank notes or travel money or include the caveat:

CurrencyFair ensures our customers at all times see the rates they are being charged along with our fee. Anyone looking to send money abroad sees the true cost of their transfer with CurrencyFair within seconds, on the CurrencyFair calculator. After all, it’s only fair.

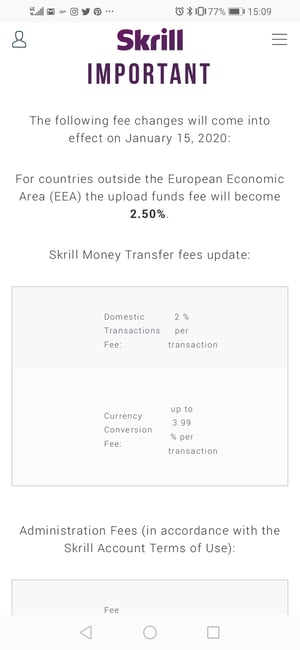

Skrill

Skrill is an online payments platform that has been in operation since 2001.

As of November 2019 they have a free trial promotion for their customers, meaning no fees on money transfers until the 15 January, 2020.

After this date, international money payments which require a currency conversion will now incur a charge of up to 3.99% of the amount transacted. As with any promotional or offer, it is usually advisable to always read the fine print.

(Gathered on 25 November 2019 at 15:09)

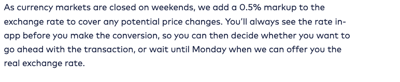

Starling

Starling joins the new range of mobile-only challenger banks mentioned in this article.

Starling charges a 0.4% of a transfer’s amount and 0.5% on the weekends to cover any price differences that occur. If the payment is made with SWIFT, there is an additional flat fee of £5.50.

(Gathered on 21 November 2019 at 15:37)

As of November 2019, there are two currencies available to deposit into a Starling bank account–Euro and Pound Sterling.

The Co-operative Bank

The Co-operative Bank is a “bank for people with a purpose”, making ethical business and practice a priority. Fees with The Co-operative Bank can range from £8 to £25 when sending money overseas with depending on the customer’s destination and desired transfer time.

(Gathered on 21 November 2019 at 15:44)

To get an “indication” of what the exchange rate will be on a money transfer with the Co-Operative Bank, it is required to call the local branch. Even so, they may adjust rates “if there are significant movements in the market”.

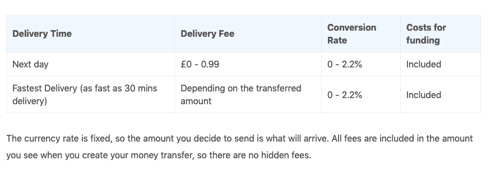

TransferGo

TransferGo is a digital remittance solution serving customers living within the EU.

TransferGo’s fees are vary depending on delivery time required and the amount being transferred. For example, sending £500 to arrive in Ireland tomorrow would cost £0.99. Sending the same amount to arrive within 30 minutes would cost £2.99.

TransferGo list their conversion rate as being from 0–2.2%– this is their margin that is being added to the currency market rate.

(Gathered on 21 November 2019 at 15:46)

CurrencyFair’s exchange margin is typically from around 0.45 %. The service of sending in GBP to your account within one hour is also available–at no extra cost. That’s currency exchange without compromise. Read more about Faster Payments here.

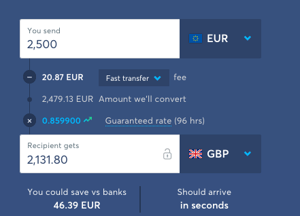

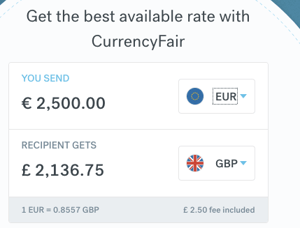

TransferWise

The fees customers pay for money transfers with TransferWise is dependent on the transfer amount, the payment method being used (bank transfer or card) and the exchange rate available on the currency market at that time.

The final amount received and paid by customers is available to view on their website before carrying out an exchange in full.

As an alternative to TransferWise, comparing a transfer of €2 500 we can see this exchanges to £2, 136.75 with CurrencyFair including our €3 fee to transfer our Euros and £2 131.80 with TransferWise to convert €2, 4179.13 including their fee of €20.87.

(Data gathered at 12:57 on 22 November 2019)

(Data gathered at 12:57 on 22 November 2019)

A feature unique to CurrencyFair customers is the opportunity to possibly exchange at a rate better than the currency market rate. This can happen in our peer-to-peer marketplace: Simply request your rate and wait for the market to match it.

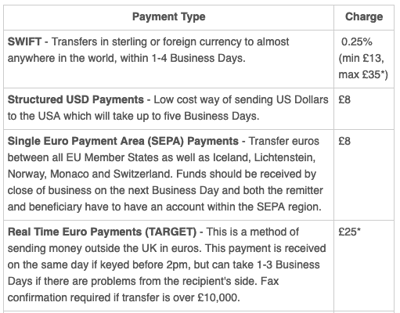

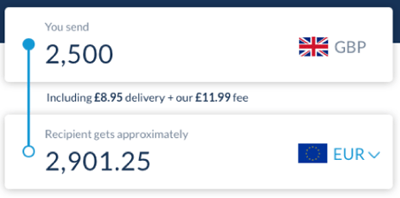

Travelex

Like MoneyCorp, Travelex also provides cash currency exchange with bureaux de change outlets located globally. The fees on their international payments service, Travelex Wire, to send money within two days of the transfer taking place is called a “Standard” transfer and is free of charge. For next day delivery, a SWIFT transfer will cost £8.95 with Travelex.

Travelex’s calculator operates using ‘indicative exchange rates’. That means, when actually placing an order, the exchange rate could change.

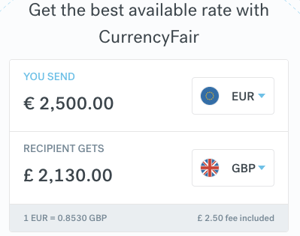

We carried out a comparison of their SWIFT, next-day service against our real-time transfers. Comparing an exchange of £2 500 to Euros we can see this exchanges to €2, 911.25 including a €3 fee with CurrencyFair and €2, 901.25 including an £8.95 delivery fee and an £11.99 fee with Travelex.

(Data gathered at 12:31 on 18 November, 2019.)

(Data gathered at 12:31 on 18 November, 2019.)

Ulster Bank

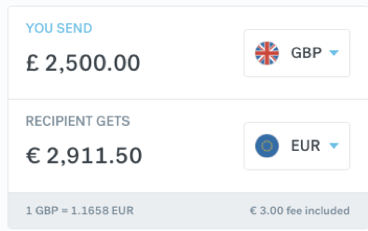

Ulster Bank is an Irish bank with branches across Ireland. Comparing their rates with CurrencyFair, we can see that the exchange rates to exchange €2 500 to Pound Sterling gave us a rate of 0.8332 with Ulster Bank and 0.8530 with CurrencyFair, so before fees, to exchange €2 500 you would receive £2 083 and £2 132.50 respectively.

That means £49.50 more with CurrencyFair and our fee to transfer out Sterling is just £2.50.

(Data for comparison gathered at 16:42 on 19 November, 2019.)

(Data for comparison gathered at 16:43 on 19 November, 2019.)

Western Union

Western Union have currency exchange outlets across the world and they also offer an online service.

To deposit by bank transfer with Western Union is free of charge. As with most providers including CurrencyFair, deposits by debit card incur a fee.

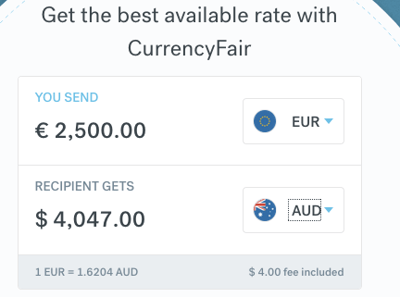

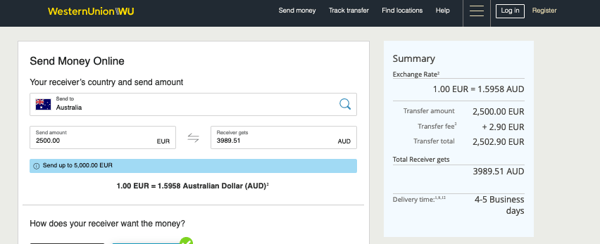

Western Union states that the margin placed on the going currency market rate is “subject to change without notice”. Comparing their exchange rates with CurrencyFair, we can see that te rate to exchange €2 500 to Australian Dollars is 1.6204 with CurrencyFair and 1.5958 with Western Union by bank transfer only. The amount received by the recipient is A$4 047 with CurrencyFair including our A$4 fee and A$3 989.51 with Western Union including their fee of €2.90. This is A$57 less with Western Union. Their transfer time is 4–5 business days whereas with CurrencyFair the transfer time is 1–2 business days.

(Data for comparison gathered at 13:30 on the 22 November, 2019.)

(Data for comparison gathered at 13:30 on the 22 November, 2019)

WorldFirst

World First is an online foreign exchange broker that has been in operation since 2004 offering online transfers to people and businesses.

The WorldFirst fee structure works by charging customers according to how much they send overseas each year. Customers that send under £500 000 in a year are charged an additional 0.5%, while customers that send £500 000 - £5 million are charged 0.25%, with the rate charged decreasing the more that is transferred.

WorldFirst only displays the currency market rate (or the rate available on Google) on their website. However the actual exchange rate charged to customers is explained to be “...subject to change”.

(Gathered at 09:42 on the 22 November, 2019.)

WorldRemit

Since 2010, WorldRemit has offered online currency exchange for personal customers. Their website states that their business account is suited to small and medium sized businesses based in the UK.

Their transfer fee varies depending on the destination of the exchanged currency. Their fee is charged in excess of the amount being transferred and WorldRemit then charges a margin on top of their exchange rate, which changes depending on the currency customers have and the currency they are exchanging to.

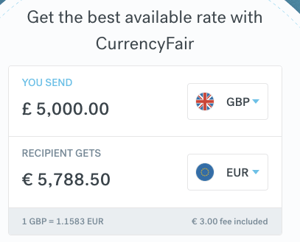

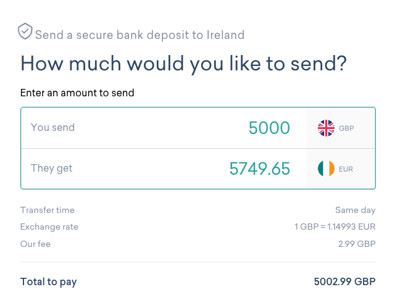

A comparison in both currency calculators to exchange £5 000 to Euros at a rate of 1.1583 resulted in € 5 788.50 with CurrencyFair, including our fee of €3 and €5 749.65 with WorldRemit, excluding their fee of £2.99 which is added to the amount transferred making the “Total to pay” with WorldRemit equal £5 502.99.

(Data for comparison gathered at 10:26 on the 22 November, 2019)

(Data for comparison gathered at 10:26 on the 22 November, 2019)

XE.com

Based in Canada, XE is a renowned online foreign exchange platform.

Their website states,

The online remittance service has a useful calculator on its homepage, with the caveat:

Their money transfer rates platform is advertised, but there is no calculator available to test and see the rates on offer for anyone who opens an account with them.

(Gathered on 22 November at 10:53)

Those looking to transfer should investigate further any claim a provider offers to be “fee-free” claim before deciding to use the service as typically the provider adds a mark-up to the exchange rate to cover the fee that is being waived. With CurrencyFair our margin is typically just 0.45-0.6% away from the currency market rate and our fee is €3 or the currency equivalent.

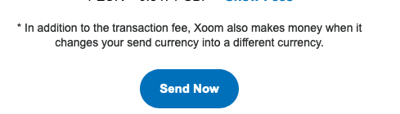

Xoom

Xoom is one of the latest offerings from PayPal giving electronic funds transfers and remittances.

The global payments platform’s cost structure is made up of fixed fees that vary according to the destination country of the payment. The money sent with Xoom can be received via a cash pickup or deposited to a bank account. Xoom customers can transfer in four currencies to be exchanged: Canadian Dollars, US Dollars, Pound Sterling and Euro. Sending Pound Sterling to Europe costs £0.99 per transfer; to Australia, £6.99; to America or India, £1.99.

Xoom’s website states,

(Gathered on 25 November at 14:56)

So there you have it - the best money transfer companies compared. We'll keep an eye on the industry and will continue to add new companies as they join the scene.

Don't forget to spread the word about CurrencyFair!